Break-even analysis

- Created by: charliedee

- Created on: 16-05-17 21:40

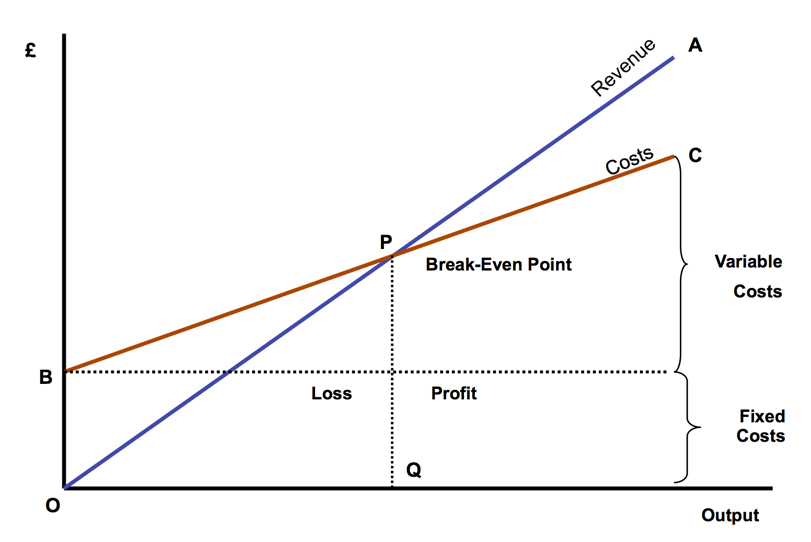

38.4 Break-even charts

A break even chart is a graph showing the revenue and costs for a business at all possible levels of demand or output. The break-even chart uses the horizontal axis to represent the output per time period for the business, for example, beteen 0 and 1000 units a month. The vertical axis represents costs and sales in £.

Margin of safety = sales - BE point.

The higher the MoS the less likely it is that a loss-making strategy situation will develop.

Comments

No comments have yet been made