Accounting Semester II

0.0 / 5

- Created by: sophiesss

- Created on: 14-03-17 18:21

Liquidity

Converting assets into cash to pay bills

1 of 74

Solvency

Have we got sufficient cash to pay the bills?

2 of 74

Financial adaptability

The ability to meet external shocks (we need cash to do this)

3 of 74

Cash

Notes and coins in hand and deposits in banks and similar institutions that are accessible on demand

4 of 74

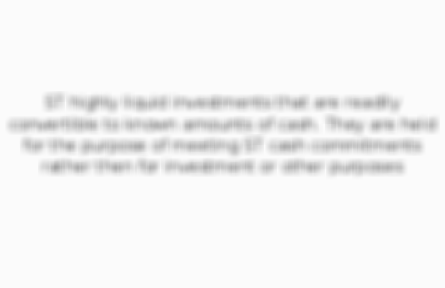

Cash equivalents

ST highly liquid investments that are readily convertible to known amounts of cash. They are held for the purpose of meeting ST cash commitments rather then for investment or other purposes

5 of 74

IAS7 cash

Cash + bank - overdraft

6 of 74

Cash inflows

Increases in cash. Monies generated from trading, commonly referred to as cash flows from operations, monies from new share issues or other forms of LT finance and monies received from the sale of a fixed asset

7 of 74

Cash outflows

Decreases in cash. Monies used to buy new fixed assets, to pay tax and dividends and to repay debenture holders or other providers of LT capital

8 of 74

Net cash flow

The net effect of cash inflows and cash outflows

9 of 74

Operating activities

The principal revenue-producing activities of the entity. Therefore, cash flows from operating activities generally result from the transactions and other events and conditions that enter into the determination of profit or loss

10 of 74

Investing activities

All payments and receipts in respect to the acquisition and disposal of a non-current asset

11 of 74

Financing activities

Anything relating to the LT financing of the business

12 of 74

Ratio

A mathematical expression of the relationship between two or more variables, there must be a significant relationship

13 of 74

Profitability ratio

Is the business making a profit? How good is the profit? Is it a good return for shareholders?

14 of 74

Efficiency ratio

Is the firm using its resources effectively to generate sales and keeping costs low?

15 of 74

Liquidity ratio

Can the firm pay its way in the short-term?

16 of 74

Gearing ratio

Is the financial structure sensible (debt/ financial risk)? Is the firm making appropriate use of borrowings? Has it struck the right balance between equity and loan finance?

17 of 74

Investor ratio

Is it attractive to a potential shareholder?

18 of 74

Return on capital employed equation (X2)

(Operating profit (PBIT)/ capital employed) X 100 OR (net profit margin x capital employed turnover ratio) x 100

19 of 74

PBIT

Profit Before Interest and Tax

20 of 74

Capital employed

Debt (LT borrowing) + equity (share capital/ premium/ retained profits)

21 of 74

Return on shareholder funds equation

(Profit after tax (earnings)/ shareholder funds) X 100

22 of 74

Gross profit margin equation (X2)

(Gross profit/ sales) X 100 OR ((sales - COGS)/ sales)) X 100

23 of 74

Net profit margin equation

(Operating profit (PBIT)/ sales) X 100

24 of 74

Capital employed turnover equation

Sales/ capital employed

25 of 74

Non current asset turnover ratio equation

Sales/ non-current assets

26 of 74

Average (debtor) collection period equation

(Trade receivables/ credit sales) X 365 days

27 of 74

Inventory holding period equation

(Inventory/ cost of sales) X 365 days

28 of 74

Payables (creditor) payment period equation

(Trade payables/ COGS) X 365 days

29 of 74

Net trade (operating) cycle equation

Stock (inventory) holding period + debtor (receivables) collection period - creditor (payables) payment period

30 of 74

Current ratio

Current assets/ current liabilities

31 of 74

Quick ratio/ acid test

(Current assets - inventory)/ current liabilities

32 of 74

Debt : equity ratio equation

(LT debt/ shareholder funds) X 100

33 of 74

Interest cover ratio equation

PBIT/ interest

34 of 74

Earnings per share equation

Profit after tax/ total shares in issue

35 of 74

Number of shares

Issued share capital/ par value of one share

36 of 74

Price/ earnings ratio equation

Current market share price/ earnings per share

37 of 74

Dividend cover equation (X2)

Profit after tax/ dividends OR earnings per share/ dividend per share

38 of 74

Budget

A plan expressed in money. It may show income, expenditure and capital to be employed. It is a forward looking document

39 of 74

Master budget

This is for the whole company, it comprises of a series of sub-budgets

40 of 74

The budget process

Refers to the sequence of operations necessary to produce a budget for a particular organization. The sequence of operations will depend upon the type of organization and its perceived requirements for planning and control

41 of 74

Sales and production budget

Normally prepared for manufacturing organizations and will reflect the respective targets for these functions in the forthcoming budget period

42 of 74

Fixed budget

Prepared on the basis of an estimated activity level (e.g. estimated volumes of production/ estimated volume of sales)

43 of 74

Flexible budget

The budget is ‘flexed’ to the actual output level whether it is higher or lower than the fixed budget. Only variable costs and sales will be affected.

44 of 74

Cost unit

A unit of production to which costs can be related. The nature of costs depends on the company. Products can also be service orientated. E.g. ships in a shipbuilders/ bread in a bakery

45 of 74

Cost centre

Separately identifiable sections of an enterprise to which costs can be related

46 of 74

Indirect (overhead) costs

Certain costs which cannot be directly linked directly to products e.g. rent/ electricity/ gas

47 of 74

Direct costs

These can be directly linked to the cost unit e.g. wheels and a car, you know you will need four wheels per car so you just need to find the cost of one wheel and multiple it by

48 of 74

Production departments

Those cost centres responsible for producing cost units e.g. those departments which make products (manufacturing) or generate fees (services)

49 of 74

Service departments

Provide service support to production departments e.g. quality control/ security/ maintenance. Service departments have no product to sell and therefore cannot recover their costs

50 of 74

Full costing

The full cost of a product consists of the direct and indirect costs of production

51 of 74

Period costs

Any costs not classified as product costs. Costs that relate to the current period in question. They are viewed as costs that cannot justifiably be carried forward to future periods because they do not represent future benefits or because the future

52 of 74

Apportioning equation

Total overheads of a production cost centre/ level of activity

53 of 74

Activity based costing

Recognizes the complexity of business activities, the nature of overheads and what drives or causes them

54 of 74

Job costing system

Used when the costs of each unit of production can be identified at any time in the manufacturing cycle

55 of 74

Process costing system

Individual products cannot be identified until the manufacturing process is complete

56 of 74

Marginal costing

Only direct production costs are included as product costs in marginal costing

57 of 74

Difference in profits equation

Fixed overhead absorption rate x the movement in inventories during a period

58 of 74

Contribution equation

Total revenue - variable costs

59 of 74

Contribution per unit equation

Selling price - variable cost per unit

60 of 74

Break-even point

The level of sales at which revenues are just sufficient to cover total costs, with neither a profit nor a loss accruing. Here total revenue = total costs (profit = 0)

61 of 74

Contribution equation

Sales revenue - variable costs

62 of 74

Postive contribution

Selling price is greater then the VC

63 of 74

Variable costs

the same per unit of activity and therefore total variable costs will increase and decrease in direct proportion to the increase/ decrease in the activity level. The activity level may be measured in terms of either production/ service output.

64 of 74

Fixed costs

a cost which doesn’t change in response to changes in the activity level

65 of 74

Linear cost functions

o The notion that one thing will depend on another according to some mathematical relation

66 of 74

The relevant range of activity

relates to the level of activity that the firm has experienced in past periods. It is assumed that in this relationship between the independent and the dependent variables will be similar to that previously experienced

67 of 74

Cost estimation

relates to methods that are used to measure past costs at varying activity levels. These costs will then be employed as the basis to predict future costs that will be used in decision making

68 of 74

Sunk costs

can be easily identified in that they will have to be paid for or are owed under legally binding contracts. The firm is committed to paying for them in the future

69 of 74

Differential costs

the differences in costs/ benefits between alternative opportunities available to the organization. It follows that when a number of opportunities are being considered, costs/ benefits that are common to these alternative opportunities will be irrele

70 of 74

Opportunity cost

the maximum benefit which could be obtained from that resource if it were used for some alternative purposes. The potential forgone benefits are a relevant cost in a decision

71 of 74

Relevant costs and benefits

those that relate to the future and are additional costs and revenues that will be incurred or result from a decision

72 of 74

Decision making with constraints objective

when there are resource constraints, the objective that should be applied is to establish the optimum output within the constraints to maximize contribution and therefore points

73 of 74

Make or buy decisions

involves the problem of an organization choosing between making a product or carrying out a service using its own resources, and paying another external organization to make or carry out a service for them

74 of 74

Other cards in this set

Card 2

Front

Solvency

Back

Have we got sufficient cash to pay the bills?

Card 3

Front

Financial adaptability

Back

Card 4

Front

Cash

Back

Card 5

Front

Cash equivalents

Back

Similar Accounting resources:

0.0 / 5

0.0 / 5

0.0 / 5

4.0 / 5 based on 2 ratings

0.0 / 5

0.0 / 5

0.0 / 5

0.0 / 5

Comments

No comments have yet been made