Production, Costs and Revenue

- Created by: ekenny5

- Created on: 14-01-21 13:58

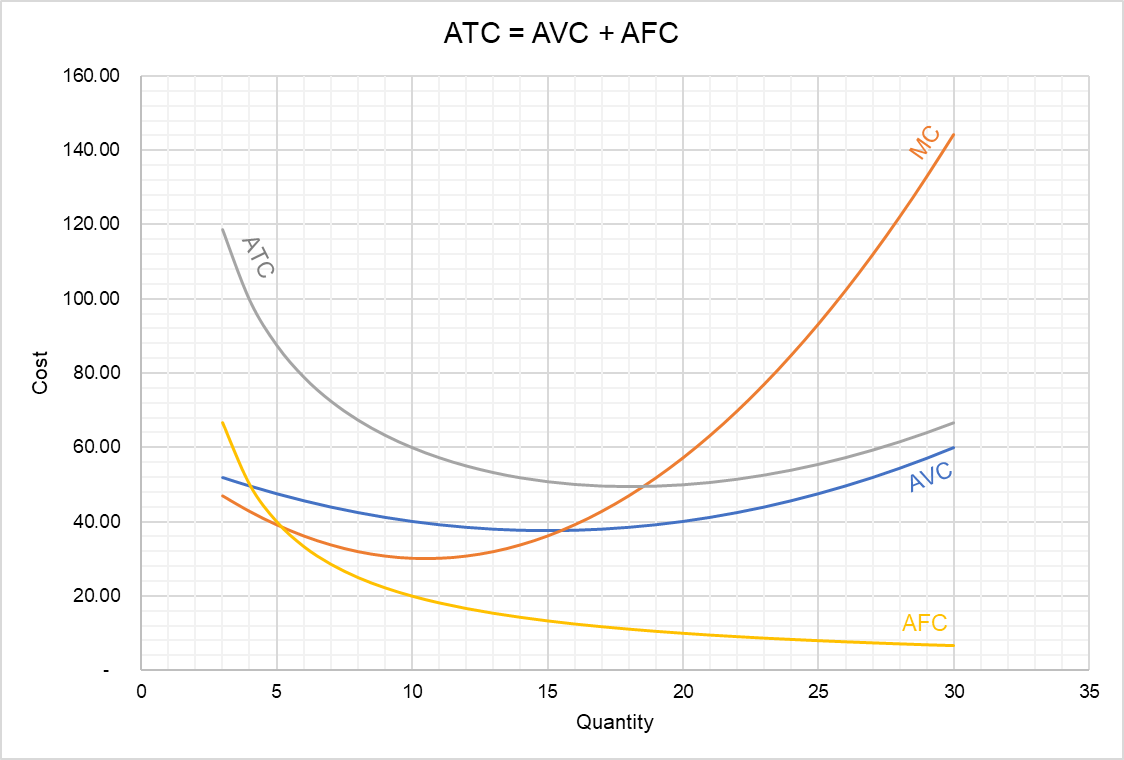

Average Cost Curves

As units increase, costs decrease (economies of scale) until all factors are used to their productive potential, at the minimum cost point (X,P). The costs then increase due to diseconomies of scale

As units increase, costs decrease (economies of scale) until all factors are used to their productive potential, at the minimum cost point (X,P). The costs then increase due to diseconomies of scale

Average Fixed Costs

The fixed costs will remain the same, but as number of units increases, the average fixed costs per unit will decrease. The fixed costs remain the same but they are spead across many more units.

Average Total Costs

Long Run Average Costs

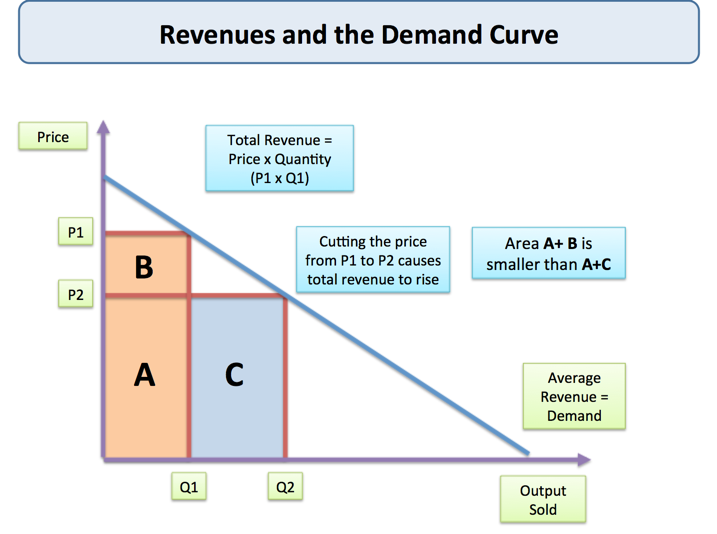

Average Revenue Curve

AR curve = demand curve

AR curve = demand curve

Comments

No comments have yet been made