Price Determination in a Competitive Market

- Created by: ekenny5

- Created on: 01-12-20 17:39

The Demand Curve

P1 Q1 is the equilibrium (ruling market price)

P1 Q1 is the equilibrium (ruling market price)

When price increases to p2, demand contracts (Q2)

When price decreases to P3, demand expands (Q3) - lower price increases demand as more affordable

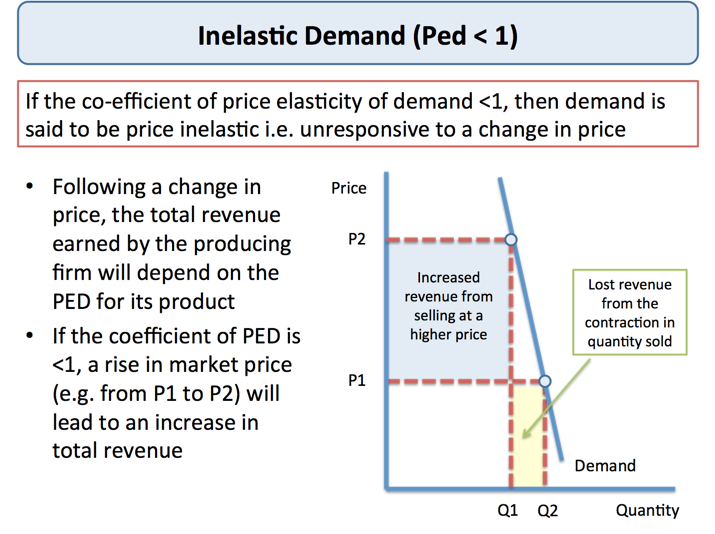

Inelastic demand (PED < 1)

goods such as life saving medicines, drugs and cigarettes (addictive), fuel, wheat, milk, rice.

goods such as life saving medicines, drugs and cigarettes (addictive), fuel, wheat, milk, rice.

A large change in price will have little effect on demand, as the goods are necessary, so will always be demanded

Elastic Demand (PED > 1)

A small change in price here (25p) has a very large impact on the change in quantity demanded (6). The demand is highly responsive to price change. The smaller box is the decrease in revenue from selling at a lower price, but the box for the increase in revenue from increased quantity is much bigger so increased total revenue.

A small change in price here (25p) has a very large impact on the change in quantity demanded (6). The demand is highly responsive to price change. The smaller box is the decrease in revenue from selling at a lower price, but the box for the increase in revenue from increased quantity is much bigger so increased total revenue.

Examples of elastic goods are cars, clothing, soft drinks

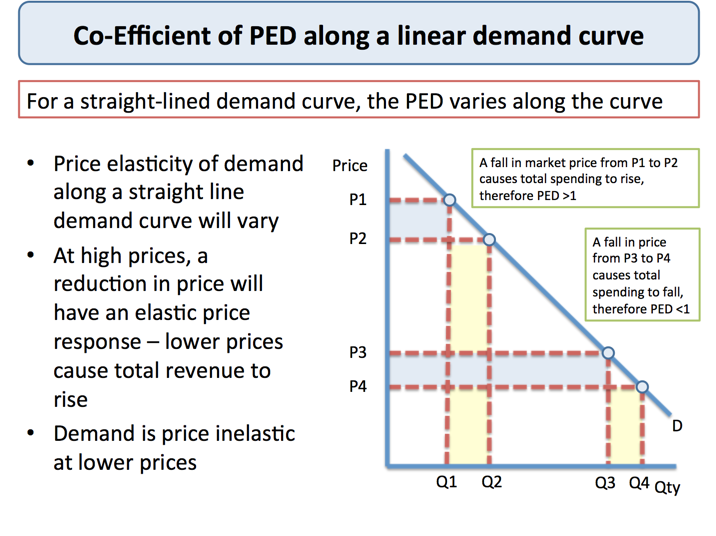

Linear Demand Curve

Unitary Demand (PED = 1)

eg electronics

eg electronics

Perfectly Inelastic Demand (PED = 0)

eg essential foods, tobacco, water

eg essential foods, tobacco, water

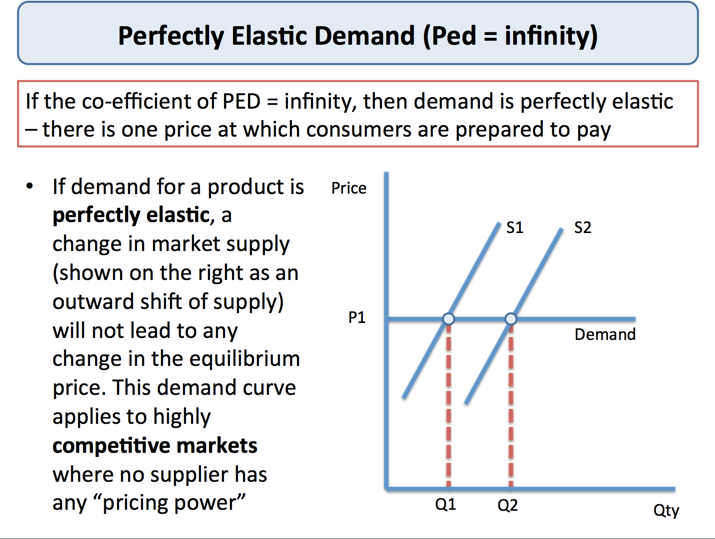

Perfectly Elastic Demand (PED = infinity)

eg products with many close substitutes

eg products with many close substitutes

Income Elastic (YED > 1)

An increase in income leads to a bigger increase in the quantity demanded of the good.

An increase in income leads to a bigger increase in the quantity demanded of the good.

These are normal goods, the demand curve will shift outward for these goods with an increase in income.

Normal necessities: low but +ve YED eg milk

Normal luxuries: high and +ve YED eg cars, technology

Income Inelastic (YED < 1)

As income increases, quantity demanded decreases

As income increases, quantity demanded decreases

Inferior goods eg own brand products or things like rice, when incomes increase, consumers will switch to more expensive/luxury goods. Inferior goods are countercyclical as they don't follow economic cycles.

Perfectly Elastic Income (0

The demand for these goods doesn't change much with a change in income. If income ^ demand barely changes, this is because they are necessities, meaning income increases won't really increase the demand for bread, as consumers already needed it

The demand for these goods doesn't change much with a change in income. If income ^ demand barely changes, this is because they are necessities, meaning income increases won't really increase the demand for bread, as consumers already needed it

Substitutes

close substitutes eg bread and cereal

close substitutes eg bread and cereal

weak substitutes are likely branded products like Apple, people are unlikley to swap

XED >1

Compliments

close compliments are like cars and fuel

close compliments are like cars and fuel

XED < 0

Supply

Supply is the quantity of a good or service that a producer is willing and able to supply to the market at a given price level in a given time

The basic law of supply is that the price of a product rises, so businesses expand supply to the market (more profit to be made)

increased market price gives a profit incentive for suppliers, so as price rises, supply expands. When output expands, costs of production tend to rise, so a higher price is needed to cover the extra costs. More entrants coming into the market at higher prices as more profit can be made (incentive)

increased market price gives a profit incentive for suppliers, so as price rises, supply expands. When output expands, costs of production tend to rise, so a higher price is needed to cover the extra costs. More entrants coming into the market at higher prices as more profit can be made (incentive)

PES Graphs

elastic supply eg pizza, bread, books inelastic supply eg farming/fishing or growing crops (takes time to increase output)

elastic supply eg pizza, bread, books inelastic supply eg farming/fishing or growing crops (takes time to increase output)

Perfectly Elastic / Inelastic Supply

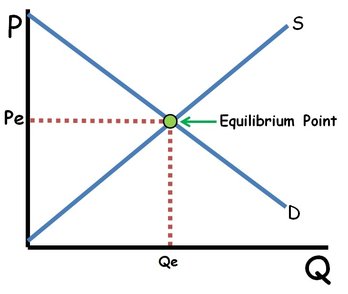

Market Equilibrium and Disequilibrium

Equilibrium means a state of equality or balance between market demand and supply. This is the price where demand and supply are out of balance are called points of disequilibrium.

Adam Smith's invisible hand links with this. meaning they work them selves out, ^ demand leads to ^ supply, and the other way around

An equilibrium is when demand = supply

The ruling market price / ruling market supply is the price where demand = supply (equilibrium)

Disequilibrium

At a disequilibrium, more is supplied than demanded, or more is demanded than supplied

- Supply - ^ price ^ supply

- Demand - ^ price decreases demand

Glut - supply > demand shortage - demand > supply

Glut - supply > demand shortage - demand > supply

Shifts in Equilibrium

Moving Equilibrium

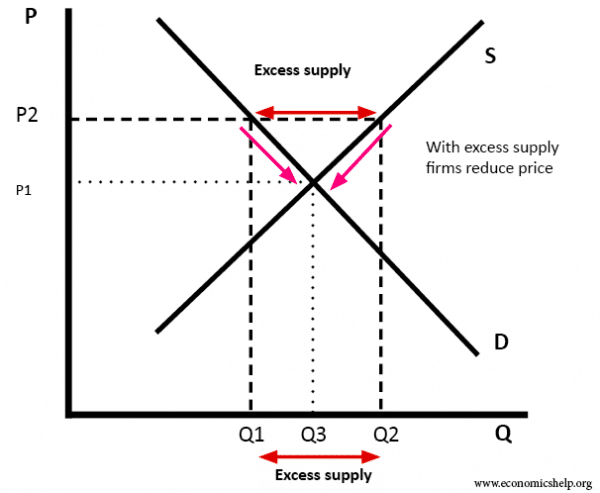

Excess Supply

This is when a market is at disequilibrium, at P2, suppliers are willing to produce Q2, but only Q1 is demanded. (Q3 is the equilibrium / market price)

This is when a market is at disequilibrium, at P2, suppliers are willing to produce Q2, but only Q1 is demanded. (Q3 is the equilibrium / market price)

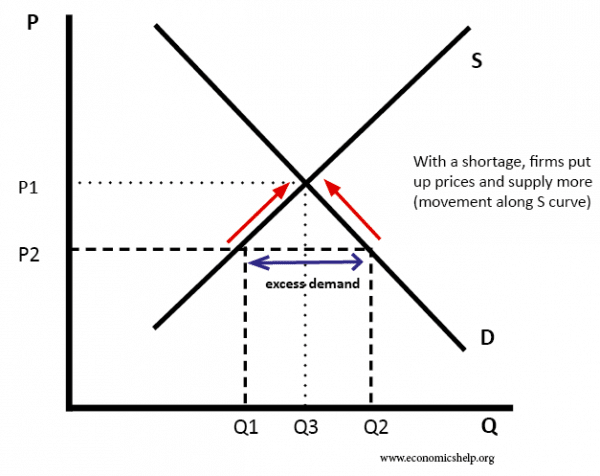

Excess Demand

At P1, there is an equilibrium, but at P2, Q1 is supplied but Q2 is demand. There is more demand than supply so excess demand.

At P1, there is an equilibrium, but at P2, Q1 is supplied but Q2 is demand. There is more demand than supply so excess demand.

The Rationing Factor

The rationing factor is when a shortage of products leads to an increase in price and deter some consumers from buying the product

Inward shift of supply increases price, so less is demanded at that price

Inward shift of supply increases price, so less is demanded at that price

The Signalling Function

The signalling function is when changes in price provide information to both producers and consumers about changes in market conditions

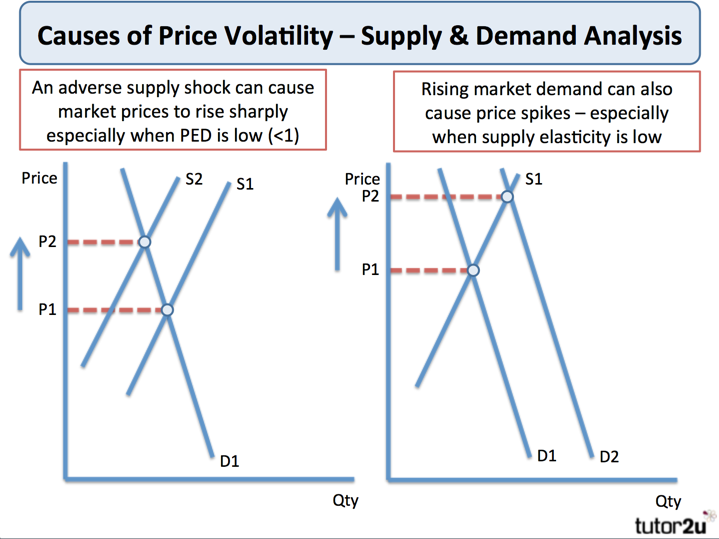

Price Volatility

Comments

No comments have yet been made