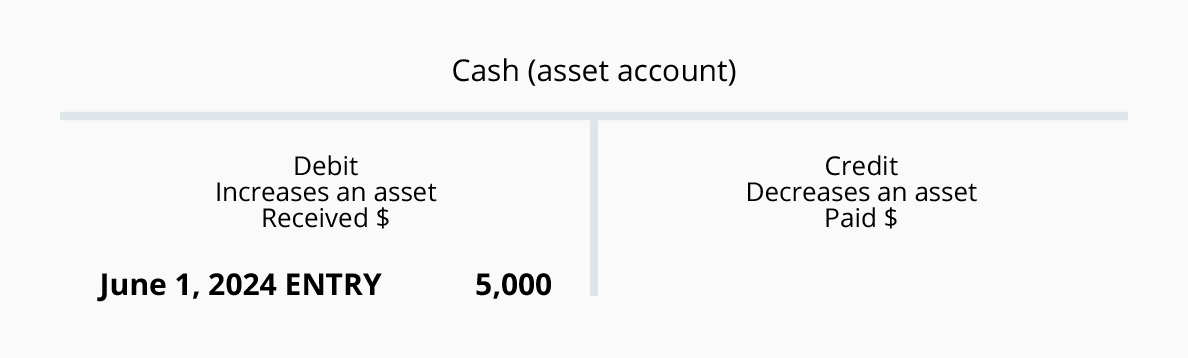

Generally these types of accounts are increased with a debit:

Dividends (Draws)

Expenses

Assets

Losses

You might think of D - E - A - L when recalling the accounts that are increased with a debit.

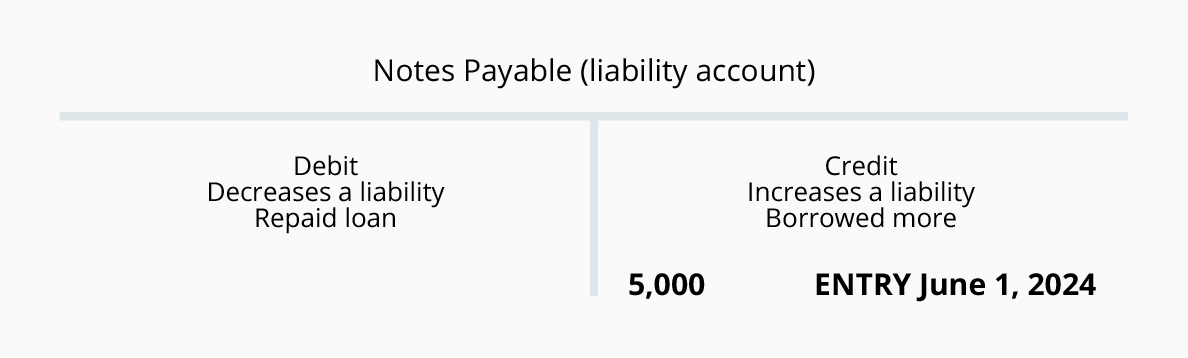

Generally the following types of accounts are increased with a credit:

Gains

Income

Revenues

Liabilities

Stockholders' (Owner's) Equity

You might think of G - I - R - L - S when recalling the accounts that are increased with a credit.

To decrease an account you do the opposite of what was done to increase the account. For example, an asset account is increased with a debit. Therefore it is decreased with a credit.The abbreviation for debit is dr. and the abbreviation for credit is cr.

Comments

Report

Report

Report