Introduction to Economics Sept 2017

- Created by: AlexK03

- Created on: 13-02-18 08:20

The demand curve

Demand- is the amount of a product that comsumers and customers are willing to pay and are able to buy at that specific point in time.

If the demand curve moves to the right = increase and left = decreae

- As the price increase the quantity demand then decreases, but if the price decreases the quantity demand increase, inverse relationship

Contraction- Demand decreases due to price increase Extension- demand increase due to price decrease

Contraction and Extension diagram & info

TO GET FULL MARKS YOU MUST LABEL AND PUT THE CORRECT ARROW:

- UP FOR CONTRACTION

- DOWN FOR EXTENSION

- AND IF THE DEMAND CURVE IS EITHER CONTRACTION/ EXTENSION DRAW ONLY ONE DEMAND CURVE LINE AND ON ARROW.

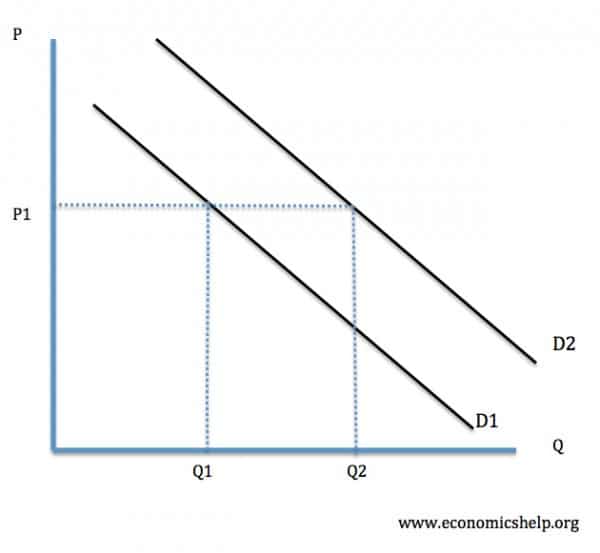

Left shift & Right shift Diagram and Info

You must label the graph and each deamnd curve line with D1 or D2 depending on whether it's right or left shift

D1 = the original demand curve

D2= the current demand curve

in the diagram above this is right shift as the outer line = right shift and the inner line = left shift

Comments

No comments have yet been made