Chapter 4. Competitive and concentrated markets. Revision notes

- Created by: Nathan890

- Created on: 13-04-17 18:16

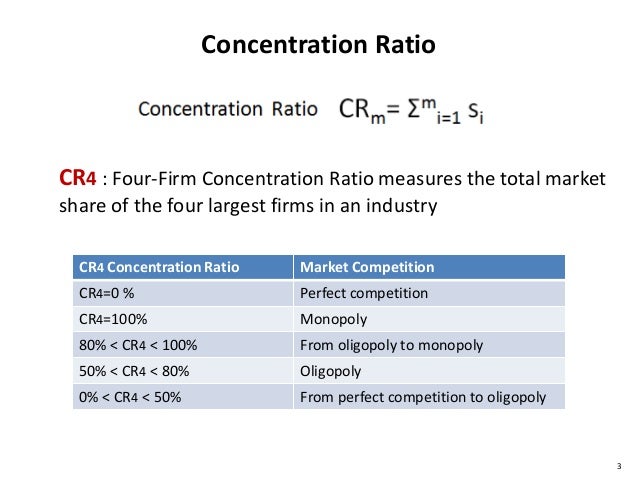

concentration ratio and market structures

Oligopoly- this is a market where there is a few firms that completely dominate it.

Resource allocation- when resources are allocated in a way which does not maximise economic welfare.

Similar Economics resources:

Teacher recommended

Comments

No comments have yet been made