Balance sheets and income statements

- Created by: charliedee

- Created on: 29-05-17 11:19

58.2 Balance sheets

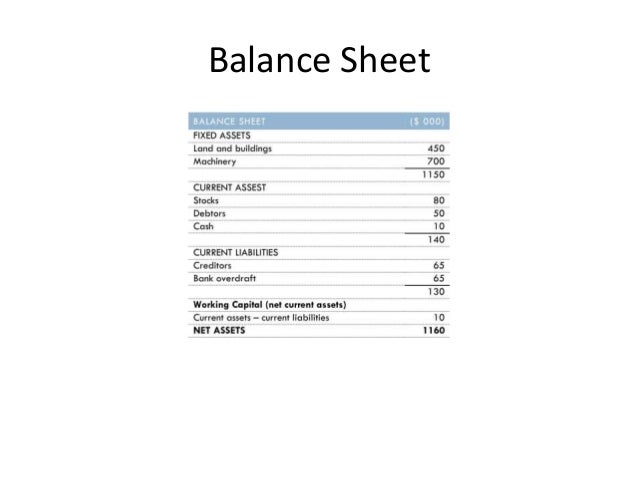

The balance sheet provides a summary of the assets and liabilities of a business. It is a snapshot of those assets at a particular moment in time.

The balance sheet shows where a business has obtained its finances - its liabilities. It also lists the assets purchased with these funds. Therefore, the balance sheet shows what the business owns and what it owes. For bankers this is of vital importance when deciding whether or not to:

- invest in a business

- lend it some money

- buy the organisation outright.

Comments

No comments have yet been made